AI is getting smarter every quarter. It can process earnings transcripts, parse filings, update models, and draft research notes in minutes. But here is a question nobody is asking: what happens when there is nothing to process?

In Vol. 5, we talked about the opinion convergence problem — how AI agents running on the same public data form the same opinions, creating new risks for markets. But that problem has a boundary. It is overwhelmingly a large-cap problem. The moment you move down the market cap spectrum, the dynamics change completely. And that is what this volume is about.

The Data Abundance Problem in Large-Caps

Large-cap companies are the most well-documented entities in the financial world. Quarterly earnings transcripts, annual reports, investor presentations, analyst days, SEC filings, proxy statements, ESG disclosures, sell-side coverage from twenty different banks, consensus estimates updated daily, management interviews on financial media. The data is everywhere, and it is all public.

This is exactly why AI works so well on large-caps. There is an enormous volume of structured and unstructured data for the models to ingest, cross-reference, and synthesise. An AI agent can read every piece of publicly available information on a company like Apple or JPMorgan in minutes and produce a reasonably coherent analysis. The raw material is abundant.

But abundant data is precisely what creates the convergence problem we discussed in Vol. 5. When every AI agent has access to the same rich dataset, they all reach similar conclusions. The edge disappears. In large-caps, AI is not a differentiator. It is table stakes.

Now Move Down the Market Cap Spectrum

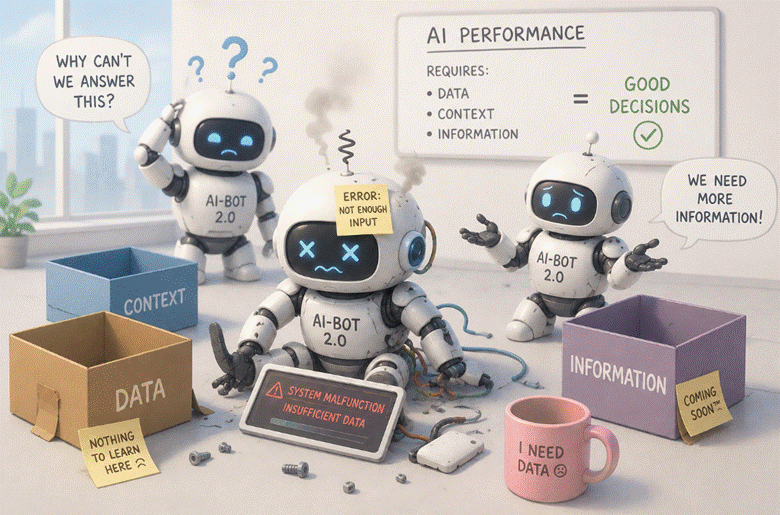

Small-caps and micro-caps are a fundamentally different universe. A $500 million company might have two sell-side analysts covering it, or none at all. Earnings transcripts are sparse. Management does not do quarterly investor presentations. There are no consensus estimates to benchmark against. The SEC filings exist, but the supplementary information that gives context — the analyst reports, the expert calls, the channel checks — is thin or nonexistent.

This is where AI hits a wall. Not because the technology is inadequate, but because there is simply not enough data to work with. An AI model that is brilliant at synthesising twenty analyst reports and five years of transcripts becomes almost useless when there is one report from three years ago and a bare-bones 10-K.

I see this regularly at SP2. Our analysts working on small and mid-cap coverage for clients spend a disproportionate amount of time on primary research — calling distributors, visiting retail locations, talking to former employees, attending industry conferences, building channel check networks. None of this information exists on the internet. None of it is available to any AI model. And it is precisely this information that drives the investment thesis.

The Widening Edge

Here is what I find genuinely interesting about this dynamic. As AI adoption accelerates, the edge in large-cap research is compressing. More firms are using AI to produce faster, cheaper coverage on the same well-documented companies. The output is increasingly similar. The alpha is disappearing.

But in small-caps, the opposite is happening. The edge is widening. Because the firms that still invest in human-driven primary research — analysts who pick up the phone, who visit factory floors, who build relationships with management teams over years — are generating insights that no AI agent can access. And as more competitors shift resources towards AI-driven large-cap coverage, fewer firms are doing this fundamental legwork on smaller companies.

The information asymmetry that has always existed in small-caps is getting larger, not smaller. And information asymmetry is where alpha lives.

Why This Is Great News for Sponsored Research Houses

There is a category of research firms that should be paying very close attention to this dynamic: sponsored research houses. These are firms that get paid by small and mid-cap companies to provide independent research coverage — the kind of coverage that most sell-side banks simply do not offer for companies below a certain market cap threshold.

Sponsored research has always had a clear value proposition: small and mid-cap companies need visibility with institutional investors, and they cannot get that visibility without quality research coverage. But in an AI-driven world, this value proposition becomes significantly stronger.

Here is why. As we discussed, AI works best where public data is abundant. For large-caps with twenty analysts covering them, AI can synthesise everything that already exists. But for a $300 million company with no sell-side coverage, there is nothing for AI to synthesise. No consensus estimates. No competing research notes. No quarterly earnings summaries from multiple sources. The information vacuum is exactly what makes sponsored research valuable — and AI cannot fill that vacuum.

A sponsored research analyst who covers a small-cap company builds a relationship with management over multiple quarters. They attend factory visits. They understand the business at a level that no AI model can replicate from public filings alone. They produce the only institutional-quality research available on that company. That research becomes the primary source of information for institutional investors evaluating the stock. In a world where AI is commoditising large-cap research, this kind of original, human-driven coverage on underfollowed companies becomes more valuable, not less.

For sponsored research firms, the strategic implication is clear: double down on what makes you unique. Your edge is not speed or scale — AI will always win on those dimensions for data-rich companies. Your edge is depth, access, and original insight on companies where you are the only source of quality research. That is an edge AI cannot erode. If anything, AI is widening it by making everything else more commoditised.

What This Means If You Are an Analyst

If you are early in your career, this should shape how you think about specialisation. The analyst who builds deep expertise in a niche sector with limited coverage — specialty chemicals, regional healthcare providers, industrial components, emerging market mid-caps — is building a career that AI cannot easily disrupt. Your value is not in processing publicly available data faster. It is in generating information that does not exist anywhere else.

The skills that matter here are the ones that have always mattered in fundamental research but are now becoming more valuable: the ability to conduct channel checks, build management relationships, triangulate data from multiple primary sources, and form a differentiated view based on information you gathered yourself. AI makes these skills more valuable, not less, because they are the skills AI cannot replicate.

What This Means If You Are Making Resource Decisions

If you are a team lead or a managing director, the temptation right now is to shift analyst headcount towards AI-augmented large-cap coverage and reduce resources allocated to small and mid-cap research. On the surface, the logic seems sound: AI makes large-cap coverage more efficient, so redeploy people there and let AI handle more of the work.

I would argue this is exactly the wrong move. Large-cap coverage is where AI gives you efficiency but not differentiation. Every other firm is making the same efficiency gain. Small and mid-cap coverage is where your human analysts generate proprietary insights that translate directly into differentiated investment views. That is where the alpha is. That is where you should be doubling down on people, not pulling them out.

The smart play is to use AI to handle the mechanical work on large-caps — data extraction, model updates, first-pass screening — and redeploy the freed-up analyst time towards deeper primary research on small and mid-caps. Let AI do what it does best on the companies with abundant data. Let your people do what they do best on the companies where data is scarce and judgment matters most.

The SP2 Perspective

At SP2, this is something we have been advising our clients on for the past year. The briefs we receive increasingly reflect this shift. Clients are not asking us for analysts to build large-cap models from scratch — AI handles much of that now. They are asking for analysts with sector expertise who can conduct primary research, verify AI-generated outputs on smaller names, and build coverage in areas where data is thin.

Our focus on qualified professionals — CAs, CFAs, MBA Finance — becomes even more relevant in this context. When you are covering a company with limited public information, you need an analyst who can read a balance sheet critically, understand working capital nuances, and identify what management is not saying. That requires deep domain expertise, not just AI fluency.

The Bottom Line

AI is transforming large-cap research. That is undeniable. But the transformation is creating efficiency, not differentiation. In small and mid-caps, where data is scarce and primary research drives the thesis, human analysts are becoming more valuable, not less. And for sponsored research houses that have always operated in this space, AI is not a threat — it is making their core offering more relevant than ever.

The firms that recognise this will allocate resources accordingly: AI for the data-rich end of the spectrum, skilled analysts for the data-scarce end. The firms that chase the AI efficiency narrative across their entire coverage universe will find themselves with undifferentiated large-cap views and neglected small-cap coverage. And in that neglected space, the firms that still do the work will find the alpha.

What Is Your Take?

Are you seeing this dynamic play out in your firm? If you run a sponsored research house, has demand for your coverage changed as AI has commoditised large-cap research? If you cover small and mid-caps, has your edge grown or shrunk as AI adoption has increased? I would love to hear how this is playing out in practice — the wins and the frustrations.

This post is published by CA Siddhartha Dongre, founder of SP2 Analytics and FootNote.AI.

SP2 Analytics provides qualified offshore research analysts (CAs, CFAs, MBA Finance) to investment banks, PE firms, VC funds, equity research shops, and consulting companies worldwide. www.sp2analytics.com

FootNote builds custom AI solutions for investment research workflows. www.aifootnote.com

If you are exploring either side of the equation — whether you need skilled analysts or want to build AI workflow tools for your team — let us talk.

Email: sid.dongre@sp2analytics.com | WhatsApp: +91 8983333940 | LinkedIn: CA Siddhartha Dongre